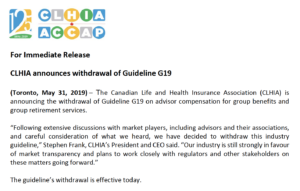

CLHIA withdrawal of G19 – May 31st, 2019

IFB/CISF Letter to CLHIA – May 29th, 2019

Insurance Journal Article – May 27th, 2019

G19 Update – May 25, 2019

There has been lots of activity and some interesting developments on G19 since we last communicated.

First of all, our industry working group has set up a website for benefits advisors (and financial advisors who want to add their voice to our opposition of CLHIA’s overreach as a trade association acting as a regulator) to register. http://groupadvisors.ca/. There are updates and information on the site and your registration will collect email addresses for future information and calls to action. We will also be using the number of registrants as an indication to regulators, politicians and CLHIA members of the scale of our group.

PLEASE CIRCULATE TO ANY FRIENDS AND ASSOCIATES IN THE BUSINESS AND AND ENCOURAGE ADVISORS TO REGISTER ASAP (even those that are not all GB or GRS, as they may be next).

Secondly, CLHIA has issued some interesting statements;

– After repeatedly indicating that G19 was the first in a line of similar guidelines that would eventually target life insurance and other individual products, CLHIA have publicly backed away from this assertion. It would be unwise for financial advisors to take this statement at face value and we should continue to encourage involvement in opposing the G19 process as a template for future CLHIA guidelines.

– CLHIA President Stephen Frank is interviewed by the Insurance Journal stating that G19 is “misunderstood”, and that it is “voluntary” for member companies to implement. The article quotes our industry group’s release that was circulated to BA members after the conference. We have since had contact with various industry publications on the matter and our position has been fairly and effectively presented in these articles.

Thirdly, we have reached out to regulators and legislators with our concerns about a trade association (CLHIA) acting as a regulator with a predictable result being harm to consumer through reduced access to independent advisors (the only target of G19). The receptiveness from these offices to our concerns has been encouraging and the interactions are ongoing. Collectively, we MUST be respectful of these offices and their roles. This means staying on message about; our support for fair, wholistic and principles based compensation disclosure; a level competitive playing field for all market participants relative to these guidelines or policies; access to independent advice for consumers; participation by all stakeholders in the process.

Lastly, there have been indications that some CLHIA members have started to push back on implementation of G19 in its current form. That is not to say that we will necessarily see changes come down the line form CLHIA but it does indicate that our collective and consistent stance is being heard and acted upon at the member company level. WE ALL NEED TO CONTINUE THESE DISCUSSIONS AT THE SENIOR LEVELS OF THE INSURERS.

We will keep members informed regularly and need your commitment. Register yourself and any of your licensed staff, then circulate the link http://groupadvisors.ca/ to all of your advisors, and ask that they register.

Insurance Journal Article – May 15, 2019

G19 Update – May 15, 2019

Our group did receive a letter on April 26th from CLHIA in response to our letter from a few weeks prior expressing our concerns around the specifics of G19 and the process CLHIA has chosen to pursue. CLHIA’s response did little to alleviate our strong concerns and the likely negative industry and consumer outcomes that G19 will cause.

We have been consistent in our position that this is not opposition to disclosure and transparency. Instead, we firmly believe that CLHIA has developed a flawed guideline with a self-serving interest. We continue to invite CLHIA to set aside G19 in favour of a true collaborative process representative of all industry stakeholders.

It is important that benefits advisors across Canada be aware and aligned on this issue. With that in mind, we have established a website at www.groupadvisors.ca where we ask advisors to register their contact information for future updates.

CLHIA Response – April 26, 2019

G19 Update – April 23, 2019

It has been some time since we provided communication on the intermediary response to Canadian Life and Health Insurance Association (CLHIA) and Guideline 19 (G19).

G19 claims to establish industry standards for the disclosure of compensation for group retirement services and group benefits. The guideline would apply to all CLHIA member companies, regardless of the form of compensation paid or provided, or the distribution channel used, except G19 is not intended to apply to insurer direct selling models or captive agents.

Much work has been done over the past several months with a primary focus on mobilizing a group representative of independent intermediaries. We are pleased to announce that this has been accomplished. Together with Advocis, CALU, TPAAC and a closely held group of benefit advisory firms, we worked on advancing our perspective and opposing G19.

In addition to the formal collaboration of our group, we have hired a consultant to formulate a cohesive strategy and consistent messaging on our G19 opposition.

Our opposition to G19 is not to be confused with opposition to disclosure. This is about opposition to a stakeholder who has no regulatory or legislative mandate to impose an industry standard. We believe CLHIA is exerting its dominant position in the marketplace in a self-serving way to the detriment of other stakeholders – specifically the consumers.

Consumers would be better served by regulation that is transparent in its making and inclusive of the interests of all stakeholders, not by one participant.

We feel opposing CLHIA actions may be the single most important issue for all intermediaries in maintaining a healthy balance in the consumer ecosystem.

Here are specific points to bring you up to date:

• The intermediary benefits community has come together in an organized fashion. This will have collateral benefits well beyond G19, such as knowledge share around other important initiatives (e.g. National Pharmacare)

• We have hired professional assistance to help navigate the complexities of CLHIA’s overstep.

• There have been countless conference calls, briefs and meetings nationally to further these discussions both with our group as well as engaging CLHIA and regulators.

• A meeting was held in mid-March between both parties (intermediary lobby group and CLHIA) to discuss current positions and explore opportunities for a revisit. This meeting did not result in any movement from CLHIA.

• A letter was sent to CLHIA President Stephen Frank and CLHIA Chair, Mark Sylvia in April outlining our position.

• We have asked for a formal response to our letter before we take the next extraordinary steps of engaging regulatory bodies, the Competition Bureau, governments and the public.

The letter presented to CLHIA on April 8th summarized various issues where G19 has overreached and some brief comments are offered as follows:

• CLHIA is not a regulator and lacks the legislative authority to make rules.

• They have used their dominant position in the marketplace to create a self-serving guideline that will harm other stakeholders.

• The imbalance created by G19 is multifaceted – unfair competition, a market distortion and a dynamic that favours CLHIA constituents including direct sales and captive agents. Moreover, G19 could lead to less access for consumers and a disruption of independent advice channels.

• The imbalance will restrict competition and could harm some stakeholders by revealing competitive information not previously

available publicly.

• The proposed G19 is not a guideline but a prescriptive set of rules that oversteps both long established International Insurance Core Principles (ICP’s) and contravenes guidance set by the Competition Bureau specific to the activities of trade associations like CLHIA. An argument can be made that CLHIA is abusing their dominant position with self-serving conduct that will undermine competitive market forces.

These points will form the foundation of our collective efforts to achieve a review of G19 and specifically the process of establishing rules of conduct for our industry going forward. Free flow of trade and an unbiased framework for competition is something we hold dear and that we must fight to preserve for all stakeholders, including consumer.

We hope this update has provided some insights on the progress we have made to bring together our collective voice and to elevate our opposition of CLHIA’s actions on this crucial consumer issue.

We will keep you informed as updates become available. This will include a future call to action as we hope to enlist your assistance as an independent intermediary as we collectively address this important issue.